DeFi Doesn't Have a Yield Problem. It Has a Borrower Problem.

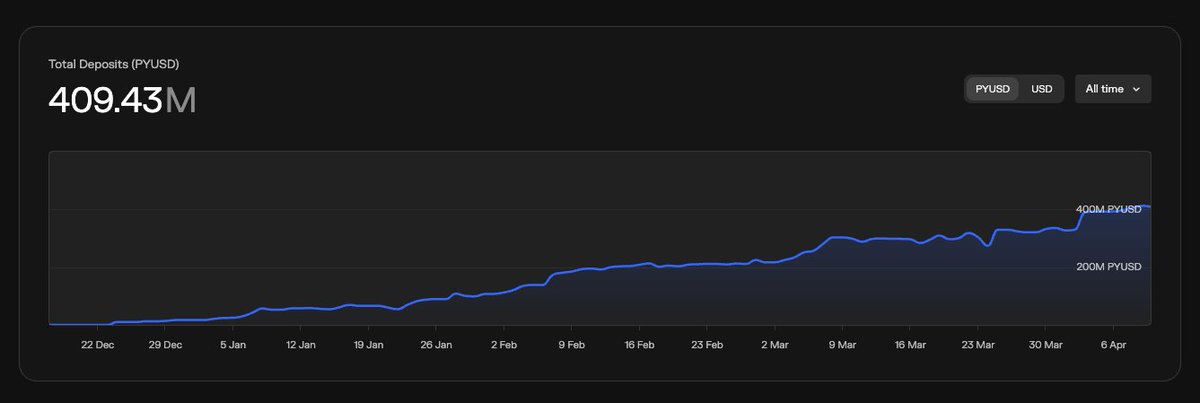

The $11.7B sitting in Morpho vaults paying 2-4% isn't a pricing error. It's the symptom of supply that was manufactured faster than demand. Here are four playbooks for fixing it.

Crypto Twitter spent this week talking about DeFi yields. The consensus: rates are too low for the risk, retail is being underpaid, the fair-value spread on ETH/BTC-collateralized lending should be 7-9% and observed rates are a fraction of that. All true. None of it explains why.The "why" is mechanical, and it's the same thing every stablecoin issuer is quietly struggling with from the other side of the order book.

Lenders are underpaid for the same reason most stablecoin issuers can't find sticky supply: organic borrow demand is the actual scarce resource, not capital.

Every dollar of subsidized stablecoin supply that enters a vault without a structural borrower on the other side compresses the rate that's supposed to compensate the lender for risk.

Most stablecoin teams treat supply growth as a marketing problem. It isn't. It's a borrower demand problem dressed up as one. You can spend $10M lighting up Morpho vaults and watch your circulating supply spike. Turn the incentives off and the capital rotates out, because it was never given a reason to stay.

The deeper issue is that lending APY is downstream of borrower demand. If nobody is borrowing your stablecoin to do something productive, the only way to keep yields up is to keep printing incentives. That's not a flywheel yet. It's a runway. And runways only matter if you use them to take off.

The reframe that fixes most of this: your stablecoin needs to be a debt asset, not a held asset.

Held assets sit in wallets and rotate to whoever pays the highest farm. Debt assets get borrowed because someone has a real reason to take on leverage in them. Every playbook below is a different way of engineering that.

So if incentives alone don't work, what does? Here are the four playbooks to grow stablecoin supply, ranked from weakest to strongest.

Playbook 1: Incentivized vaults (the bootstrap, not the destination)

Incentives are the most common playbook because they're the only one that works on day one. They get you from zero to a live market faster than anything else on this list. They just can't be the whole strategy, because incentives buy attention, not loyalty. Everything else in this article is about what you build during the window the incentives create.

You incentivize a Morpho or Euler vault, you get TVL, you get deposit count, you get a live market with real depositors. That's the win. The trap is treating that win as the finish line. The moment you stop paying, the capital rotates out, because you never gave it a structural reason to stay.

The right way to use incentivized vaults:

1. As a launching pad, not a destination. Run them to seed liquidity in markets where you eventually want organic demand. The incentive is the cost of getting the first integration live.

2. In service of one of the other playbooks. Incentivize a vault that pairs your stable with an RWA collateral so the early loopers get a kickstart. Incentivize the vault behind your overlay strategy so the first depositors see attractive APY.

3. With a defined exit. Set the date you turn the incentives off. If TVL collapses on that date, you didn't build anything. You rented depositors. That's a signal to fix the underlying demand, not to extend the program.

Treat incentives the way a startup treats paid acquisition: useful for breaking out of zero, dangerous as a permanent strategy.

Playbook 2: The overlay strategy (supply expansion without selling)

Some issuers can't or won't burn cash on incentives. They still need a way to grow supply. The overlay strategy is the cleaner alternative.

The mechanic:

1. A user deposits your stablecoin into a vault.

2. The vault uses it as collateral to borrow USDC.

3. The borrowed USDC is farmed in mature DeFi yield strategies.

4. All yield is swapped back into your stablecoin and credited to the depositor.

Two things to notice. First, the user's principal stays in your stablecoin. You're not swapping out of it to chase yield, which would be supply-contractive. Second, every cycle of yield generation buys more of your stable on the open market, which is supply-expansive at the margin.

The growth rate is lower than aggressive incentives. But the capital is sticky because the user is holding a yield-bearing version of your stablecoin, not chasing a points program. And it's repeatable indefinitely because you're not paying for it out of your own treasury. DeFi yields fund it.

This is the playbook for issuers who want growth without a cash-burning war.

Playbook 3: RWA looping

Now we get to the playbooks that produce structural demand. RWA looping is the strongest one most issuers can actively engineer, and the one most don't run because it requires partnerships, not just a budget.

The mechanic:

1. Partner with an RWA issuer (private credit, T-bills, reinsurance, remittance financing, anything yielding off-chain).

2. Their RWA token gets listed as collateral in a lending market that uses your stablecoin as the borrowable asset.

3. A user mints the RWA, posts it as collateral, borrows your stablecoin against it, mints more RWA with the borrowed stablecoin, posts that, borrows again. Loops until capital efficiency runs out.

What just happened: every loop mints new circulating supply of your stablecoin and expands the RWA issuer's balance sheet. Both sides win on their primary KPI in the same transaction. There's no zero-sum trade-off.

The borrower demand is real and it's structural. The looper isn't farming a points program. They're earning the spread between the RWA yield and the borrow rate on your stable, and they have a reason to keep that position open as long as the spread exists.

The unlock is the partnership. You need an RWA counterparty willing to use your stable as the looping asset instead of USDC. That's the work.

One caveat: not every RWA issuer is a viable partner for looping. Diligence matters, and so does upfront clarity on first-loss capital and redemption mechanics. Pick carefully.

Playbook 4: Be the default stablecoin on a chain with native borrower demand

This is the strongest playbook on the list, and the one you can't really execute through a vault. You execute it through chain-level positioning, years before the lending markets exist.

The mechanic:

Win the canonical-stablecoin slot on a chain that turns out to have organic leverage demand. Every borrower on that chain defaults to your stable. You don't pay for the demand. You don't engineer it. You just collected it by being the default unit of account in a market where people have real reasons to borrow.

There's no looping. There's no overlay. There's no incentive budget. The lending APY on your stablecoin is set by actual borrowers paying actual rates because they want leverage on something real.

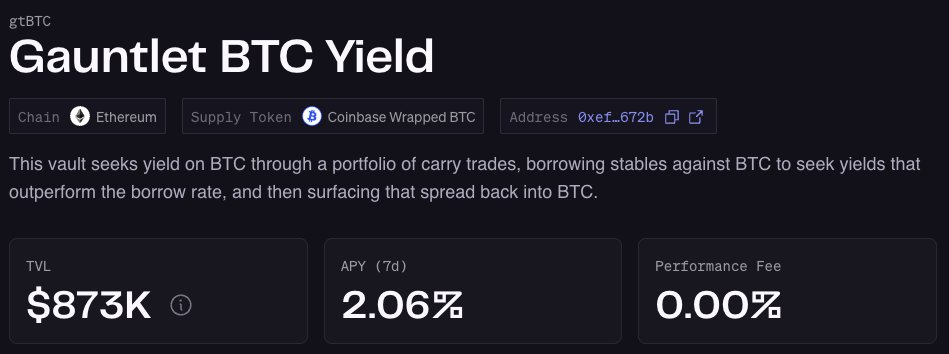

This is the example of USDT0 on HyperEVM. HYPE holders and HyperEVM-native asset holders want leverage. They post their assets as collateral on Felix and borrow USDT0 against them. That borrow demand sets the rate. Depositors collect the spread.

USDT0 didn't build that demand. It inherited it by being the canonical stablecoin on a chain whose native ecosystem generates real, structural borrower appetite. USDC on Base is arguably the same pattern at a different scale. So is USDT on Tron for remittance flows.

This is the rarest playbook because it requires being early to a chain that turns out to matter. You can't fake your way into it with a partnership or an incentive program. But when it works, it produces the cleanest sticky supply on the list: no subsidies, no engineered loops, no overlay swaps. Just borrowers borrowing because they need to.

Key takeaways

If you're growing a stablecoin or planning to launch one, and want to build a sustainable supply:

1. Audit where your borrower demand is supposed to come from. If you can't name the user and the trade, you don't have demand.

2. Stand up an overlay vault as your default product. It's your sticky-supply baseline. Every other strategy stacks on top of it.

3. Find one RWA counterparty. You only need one good looping partner to prove the mechanic. Private credit, onchain T-bills, reinsurance: any of them work if the spread is there.

4. Phase your incentive budget, don't cliff it. Spend it deliberately, on seeding the vaults, and taper as organic demand builds. The job of the program is to convert incentivized users into repeat users.

5. Pay attention to which chains are generating organic borrower demand. That's where the next USDT0-style outcome happens. Being the default stable on the right chain at the right time beats every other playbook combined.

The bigger picture

Incentives are the distribution layer for stablecoin supply. They are necessary, they are powerful, and they are the only way most stablecoins get past zero. But distribution without product-market fit is a treadmill. The job of an incentive program is to buy you the time and the attention to find the borrower demand that will eventually outlast the incentive.

The stablecoins that win the next cycle won't be the ones with the biggest incentive budgets. They'll be the ones who used those budgets deliberately, in service of a borrower-demand strategy that was always meant to outlive the program.

Emphasize your product's unique features or benefits to differentiate it from competitors

In nec dictum adipiscing pharetra enim etiam scelerisque dolor purus ipsum egestas cursus vulputate arcu egestas ut eu sed mollis consectetur mattis pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus mauris aliquam ornare nisl purus at ipsum nulla accumsan consectetur vestibulum suspendisse aliquam condimentum scelerisque lacinia pellentesque vestibulum condimentum turpis ligula pharetra dictum sapien facilisis sapien at sagittis et cursus congue.

- Pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus.

- Justo urna nisi auctor consequat consectetur dolor lectus blandit.

- Eget egestas volutpat lacinia vestibulum vitae mattis hendrerit.

- Ornare elit odio tellus orci bibendum dictum id sem congue enim amet diam.

Incorporate statistics or specific numbers to highlight the effectiveness or popularity of your offering

Convallis pellentesque ullamcorper sapien sed tristique fermentum proin amet quam tincidunt feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

Use time-sensitive language to encourage immediate action, such as "Limited Time Offer

Feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

- Pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus.

- Justo urna nisi auctor consequat consectetur dolor lectus blandit.

- Eget egestas volutpat lacinia vestibulum vitae mattis hendrerit.

- Ornare elit odio tellus orci bibendum dictum id sem congue enim amet diam.

Address customer pain points directly by showing how your product solves their problems

Feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

Vel etiam vel amet aenean eget in habitasse nunc duis tellus sem turpis risus aliquam ac volutpat tellus eu faucibus ullamcorper.

Tailor titles to your ideal customer segment using phrases like "Designed for Busy Professionals

Sed pretium id nibh id sit felis vitae volutpat volutpat adipiscing at sodales neque lectus mi phasellus commodo at elit suspendisse ornare faucibus lectus purus viverra in nec aliquet commodo et sed sed nisi tempor mi pellentesque arcu viverra pretium duis enim vulputate dignissim etiam ultrices vitae neque urna proin nibh diam turpis augue lacus.

Leandro Schlottchauer

CO-Founder & CEO, Fuul

Passionate about building and scaling products for the next web.

.png)